Hello. Welcome to Plucky Money.

My name is Plucky, and this little corner of the internet is for one reason. I want to talk about money in a way that does not make you want to crawl under the covers. No judgment. No confusing jargon. Just honest talk and simple steps to help you get control. Money is not the enemy. Feeling powerless is. So let’s start there. Let’s get you your power back.

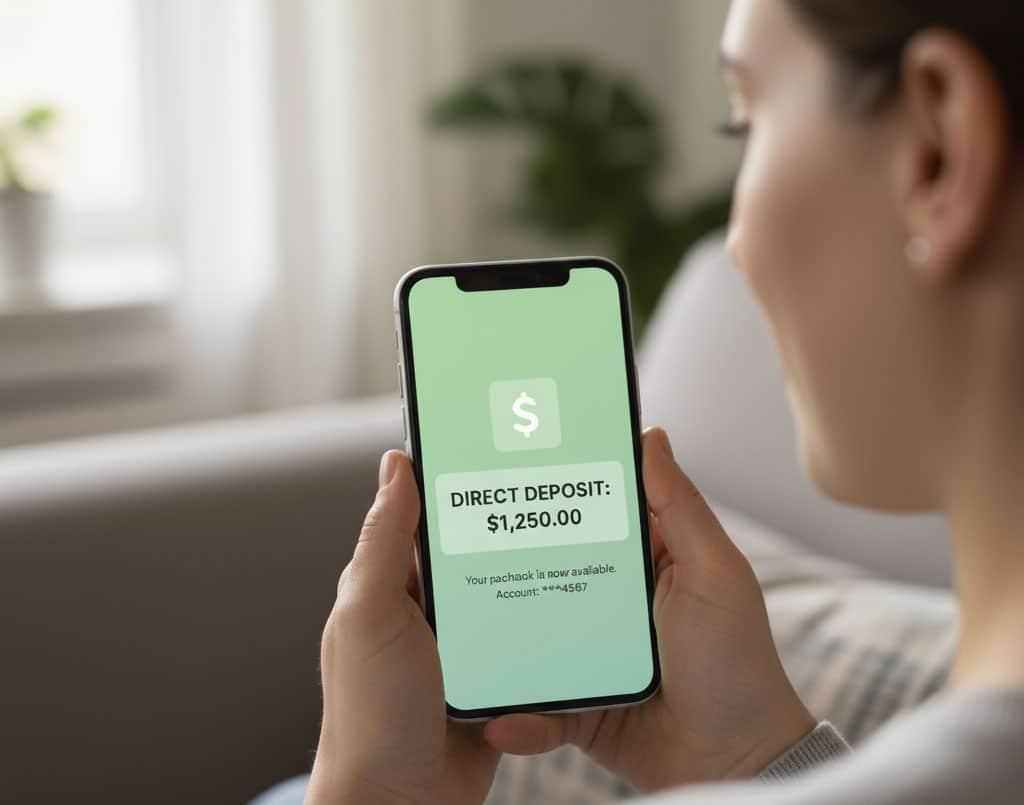

That feeling. The notification pops up on your phone. Your direct deposit has landed. A wave of relief washes over you. For a moment, you can breathe.

Then, reality hits. The rent is due tomorrow. The car payment is already scheduled to come out. Your credit card bill is staring at you from the kitchen counter. Within 24 hours, that wave of relief is gone. A huge chunk of your paycheck has vanished. You are left with just enough to scrape by until the next deposit.

Sound familiar?

You are not alone. Millions of people are caught in this exact cycle. It is the paycheck to paycheck trap. It is exhausting, stressful, and it makes you feel like you are failing. I am here to tell you that you are not failing. The system is just tricky. But you can learn the tricks to beat it.

It’s Not a Moral Failing

First, let’s get one thing straight. Living paycheck to paycheck does not mean you are bad with money. It often means your expenses are high and your income is stretched thin.

Think about it. The three biggest expenses for most households are housing, transportation, and food. These costs have grown much faster than wages over the last few decades. In many cities, rent alone can eat up 40% or even 50% of your take home pay. That does not leave a lot of room for anything else.

So please, let go of the shame. This is not about you being irresponsible for buying a coffee. This is about your money needing a clear plan to follow.

[PLACE FOR GRAPH/CHART]

You Can’t Manage What You Don’t Measure

Most people think the first step is to make a strict budget. I disagree. A budget without information is just a wish list. It feels like a cage because you have no idea what is realistic.

The real first step is tracking.

For the next 30 days, I want you to simply be a detective. Your mission is to find out where every single dollar goes. Do not judge it. Do not change anything yet. Just observe and record.

Use a notebook. Use your phone’s notes app. Use a simple tracking app. It does not matter how you do it. Just do it.

- $5.75 for that morning coffee? Write it down.

- $49.99 for that video game you bought on impulse? Write it down.

- $12.40 for lunch from the cafe near work? Write it down.

- $1.99 for that app subscription you forgot you had? Write it down.

At the end of the month, you will have something powerful. You will have data. You will see the truth, in black and white. You might think you spend $150 a month on groceries, but the data might show you it is actually $450. That discovery is not a reason to feel bad. It is a reason to feel hopeful. Now you know the truth. Now you can make a real plan.

[PLACE FOR INSPIRATIONAL QUOTE]

Your Three-Step Escape Plan

You have your data. You see where the money is going. Do not get overwhelmed and try to fix everything at once. That is a recipe for burnout. Instead, start small. So small it feels almost too easy.

Here is your plan.

- Find the One Thing. Look at your spending list. What is the one category that genuinely surprises you? Is it takeout? Is it the multiple streaming services? Is it those little trips to the convenience store? Pick just one of those categories. Your only goal for the next month is to reduce spending in that single category by 20%. If you spent $200 on Uber Eats, your goal is to spend $160 next month. That is it.

- Automate Your First Dollar. The single most effective way to save money is to make it disappear before you can spend it. Open a separate high-yield savings account. Call it your “Freedom Fund” or “Emergency Stash.” Set up an automatic transfer from your checking account for the day after you get paid. How much? Start with $25. Or $10. The amount does not matter as much as the habit. Automating this makes saving a non-negotiable expense, like your rent.

- Plan Your “Uh Oh” Money. Unexpected costs are what keep people trapped. Your tire goes flat. Your kid gets sick. These things are not really emergencies; they are just life. Assign some of your money to a “Life Happens” category. When you start building your savings, having even $500 set aside can be the difference between a minor annoyance and a full-blown financial crisis.

[PLACE FOR INFOGRAPHIC]

This is it. This is how you start. You do not need a complicated spreadsheet or a finance degree. You need to look at the truth without judgment. You need to make one small change. You need to pay yourself first, even if it is just a tiny amount.

You have lived with the stress of the paycheck to paycheck cycle for a long time. It will take some time to build a new path. The goal is not perfection. The goal is progress. You are building a buffer, one dollar at a time. This gives you breathing room. This gives you choices.

You can absolutely do this.

Citations:

- U.S. Bureau of Labor Statistics. (2024). Consumer Expenditures – 2023.

- Board of Governors of the Federal Reserve System. (2024). Report on the Economic Well-Being of U.S. Households in 2023.